Like what I saw in the year 2000, many investors are now touting the benefits of an all-equity retirement portfolio. I thought it would be fun to see how a hypothetical $2 million retirement portfolio would have performed using the 4% rule for retirement distributions and SPY ETF as the retirement investment.

The Study

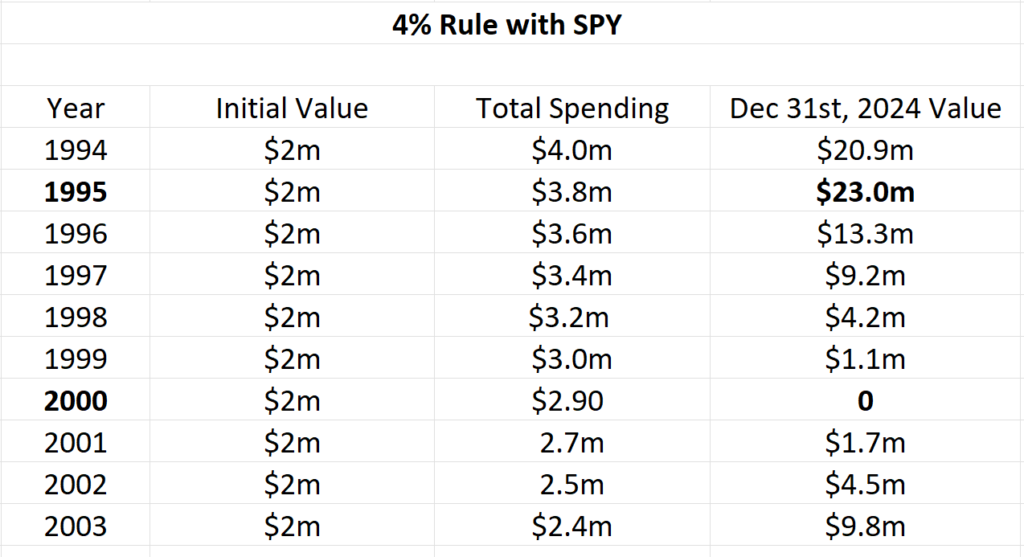

For my analysis, I ran ten different retirement start dates between 1994 – 2003. Each illustration started with a $2 million retirement portfolio invested entirely in SPY. Each illustration and hypothetical retirement date began on January 1st. Using the 4% rule, $80,000 was distributed for retirement spending in the first year. Every year thereafter, the retirement distribution was raised by 3% for inflation. All illustrations ended on December 31st of 2024.

The Results

Using the 1994 – 2003 date range allows us to see the impact of good timing, bad timing, and sequence of negative returns. This date range also gives us a realistic retirement period to study. For example, a person who retired in 1995 would be thirty years into retirement by the end of 2024. A standard retirement is 25 – 30 years in duration.

Getting Lucky – Great Timing

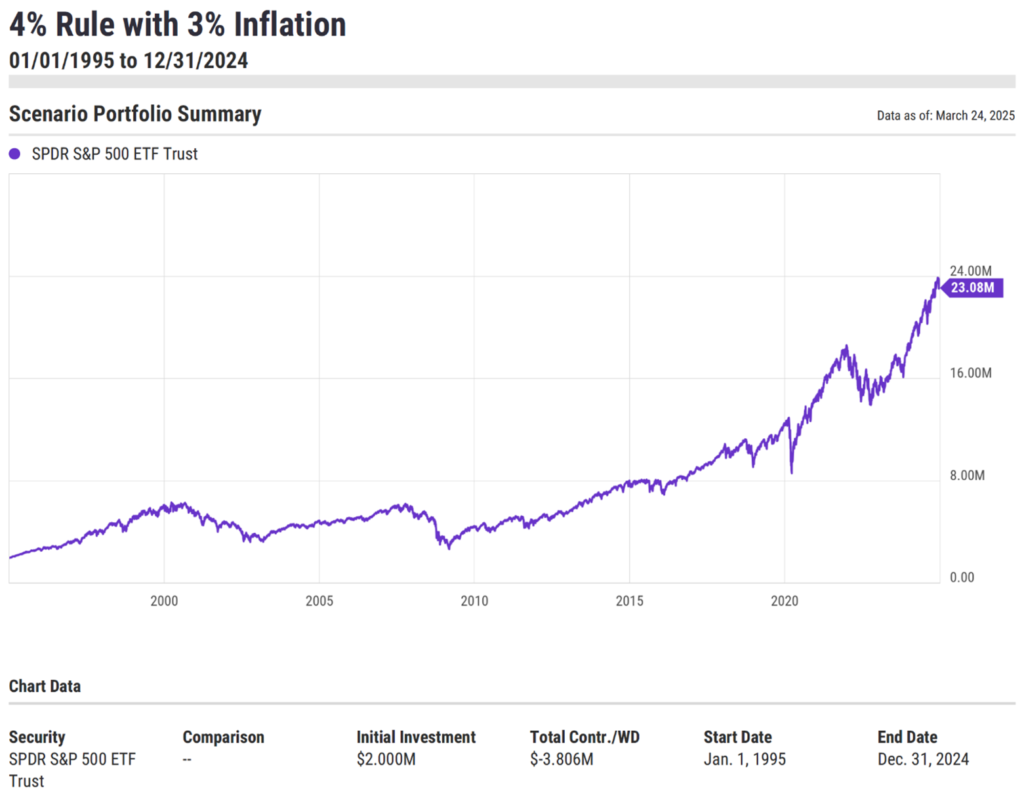

The person who retired in 1995 and invested $2 million in SPY had great timing! After thirty years, their investment was worth $23 million and along the way they spent $4 million using the 4% rule. What a retirement!

Getting it Wrong – Bad Timing

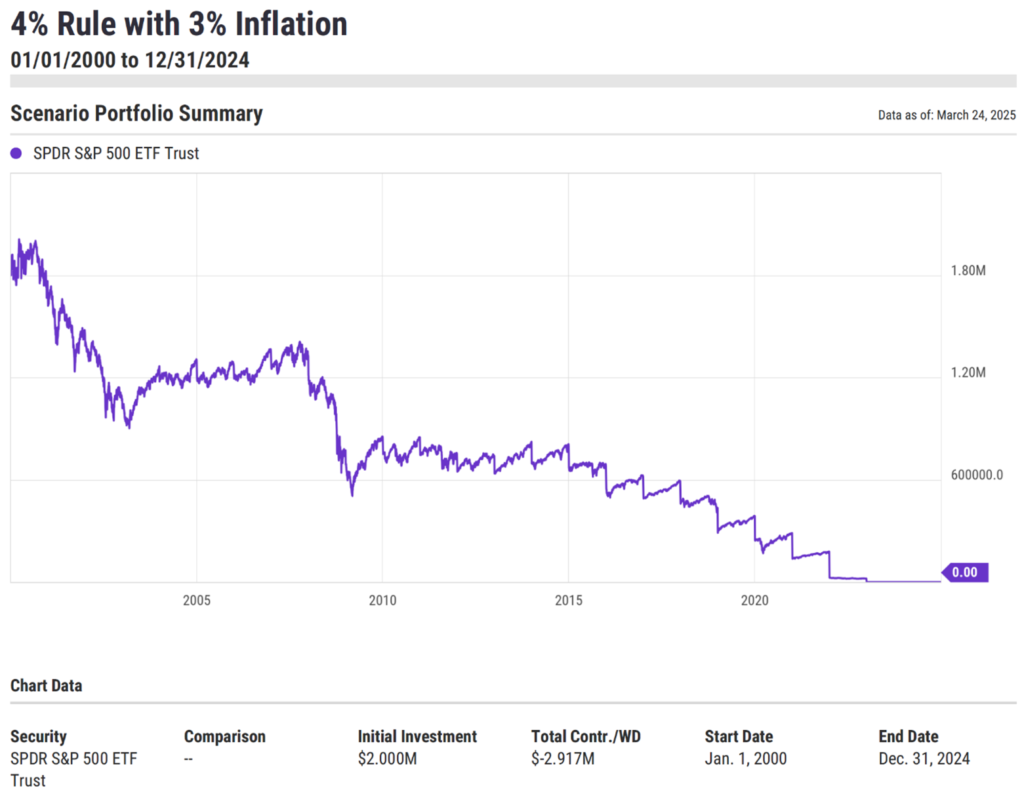

The person who retired in the year 2000 had bad timing. Retiring right before the recession of 2001 and the three-year sequence of negative returns between 2000 – 2002 was too much for an all-equity portfolio. By 2023, this retiree ran out of money.

Summary

Our analysis shows that nine out of ten hypothetical $2 million dollar retirements still had money at the end of 2024. Only one retirement date, the year 2000, ran out of money. Several of the retirements like 1994, 1995 and 1996 were able to create significant wealth during retirement and grow their nest egg well above inflation.

If you have good timing in retirement, using the 4% rule with SPY could work out great. But if you have bad timing in retirement, using the 4% rule with SPY could result in running out of money. The problem with bad timing is that you won’t know you had bad timing until it is too late!

In my experience very few retirees have the risk tolerance to maintain an all-equity portfolio in retirement. But for those who can, there can be significant long term wealth creation potential. You just need to be comfortable with the risks.

If you have questions about your investments, please give us a call, we would be happy to give you a free second opinion on your portfolio.

Ethan S. Braid, CFA

President

HighPass Asset Management

Denver, CO

This article is for education and illustrative purposes and is not tax, legal or financial advice. Your broker or advisor will charge you fees or commissions to make investments and therefore your returns will be less than indexes. For example, if you invest in the S&P 500 ETF, SPY, you will pay a fee to the company managing the ETF, State Street Global Advisors. Your return on the S&P 500 ETF, SPY, will be less than the SS&P 500 Index TR because of the fee paid to State Street Global Advisors. Additionally, you may pay a fee or a commission to your broker or financial advisor, further reducing your return, below the index. Consult your advisor or broker for a detailed list of their fees or commissions before you invest. Investing involves risk and you can lose money.