How reliable is the 4% rule when using a 60/40 equity/fixed balanced investment strategy? Will you run out of money if you have bad timing and retire right before a recession? How will sequence of negative returns affect your retirement plan? To answer these questions and more, I have created a hypothetical illustration for a person who retired on January 1st of the year 2000 with $2 million invested in the Vanguard Balanced Index Fund. The Vanguard Balanced Index Fund is a popular 60/40 equity/fixed asset allocation fund.

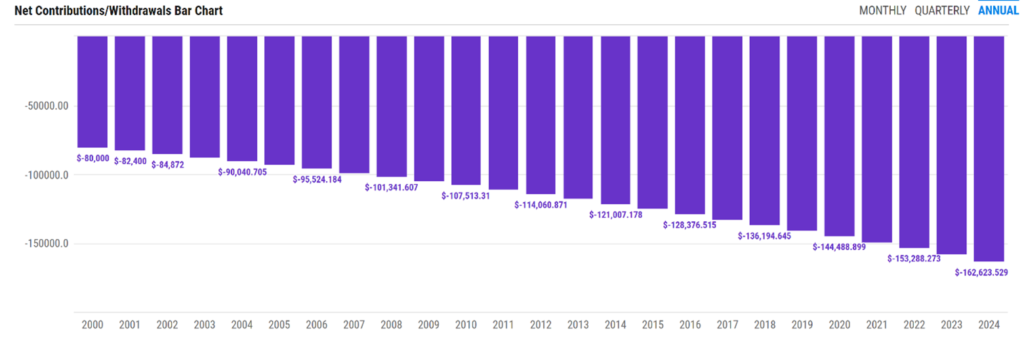

4% Rule Distributions Over 25 Years

Our retiree distributed $80,000 in the first year of retirement and then increased the distribution by 3% every year for inflation. The chart below shows the effect of inflation over the course of a twenty-five-year retirement period. At a 3% inflation rate, our retiree would need $162,623 dollars in 2024 to equate to $80,000 annual spending in the year 2000.

Investment Performance

The chart below shows our retiree’s long-term results for the Vanguard Balanced Index Fund, Admiral share class. After twenty-five years of retirement, our retiree still has $1.6m in his portfolio. All his spending needs were met with a total of $2.9m being distributed from the portfolio over twenty-five years.

Summary

The year 2000 was a bad time to retire. The S&P 500 had negative returns for 2000, 2001 and 2002. The recession of 2001 was particularly painful for technology stocks. Eight years after he retired, our retiree was hit with a second recession and stock market crash in the year 2008. Despite bad timing, sequence of negative returns and multiple recessions, our retiree was able to cover all spending needs using the 4% rule with a 60/40 equity/fixed balanced mutual fund. Due to bad timing, our retiree was not able to achieve growth of his principal and as a result, in the later stages of his retirement his portfolio is worth less than what he started retirement with.

If you have questions about your investments, please give our office a call, we would be happy to give you a free second opinion on your portfolio.

Ethan S. Braid, CFA

President

HighPass Asset Management

Denver, CO

This article is for education and illustrative purposes and is not tax, legal or financial advice. Your broker or advisor will charge you fees or commissions to make investments and therefore your returns will be less than indexes. For example, if you invest in the S&P 500 ETF, SPY, you will pay a fee to the company managing the ETF, State Street Global Advisors. Your return on the S&P 500 ETF, SPY, will be less than the SS&P 500 Index TR because of the fee paid to State Street Global Advisors. Additionally, you may pay a fee or a commission to your broker or financial advisor, further reducing your return, below the index. Consult your advisor or broker for a detailed list of their fees or commissions before you invest. Investing involves risk and you can lose money.