Today we are going to look at the differences between a fee-only vs fee-based advisors.

I am writing this article for all of you who are working with someone who tells you they are fee-based and they are probably ripping you off, hiding their commissions, selling you products, and you do not know it. I am going to show you how to determine if someone is not being transparent with you.

I am going to review some fee illustrations to demonstrate to you just how significant the conflict of interest can be when you’re working with someone who says they are fee-based. In this article I will review five fee illustrations covering annuities, private REITS, structured products, private equity, and hedge funds.

About 90% of financial advisors are dual registrant advisors who often say that they are fee-based and they often misrepresent their fiduciary obligation to you, the consumer.

Unfortunately, there are a lot of people who are working with someone that they trust and are being taken advantage of, and they just don’t know it. A fee-based advisor is nothing more than a realtor in disguise; capable of receiving all sorts of hidden commissions. A fee-based dual registrant financial advisor typically has a series 65 investment adviser license, a series 7 stockbroker license, and often has an insurance license too.

Let’s look at some fee calculations so that you can see what a fee-based advisor can hide from you.

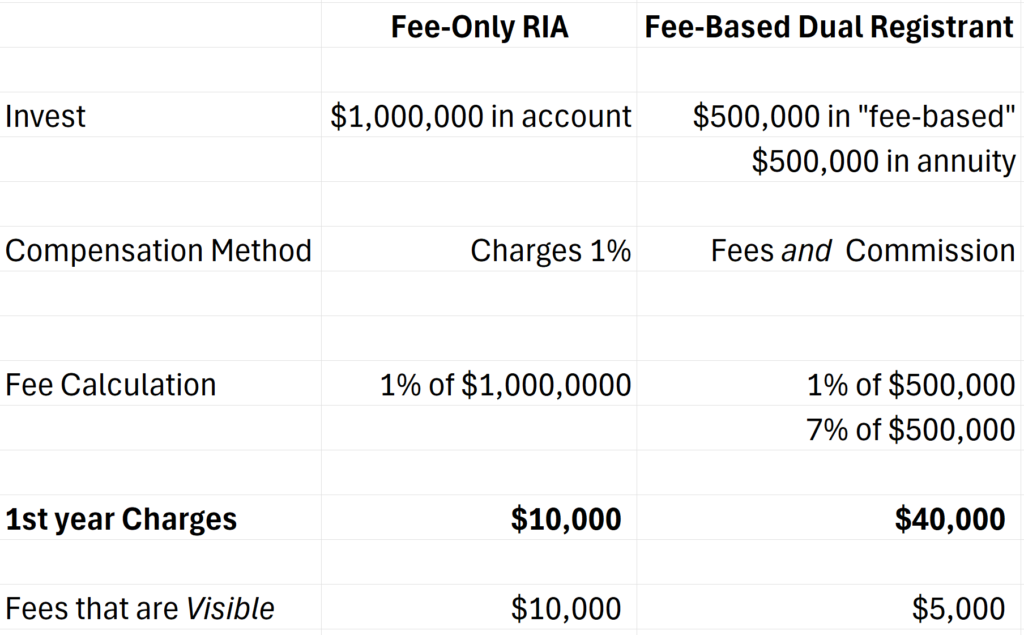

Fee-Based Financial Advisor Selling Annuities

In the table above we are giving $1,000,000 to each advisor and comparing the potential fees. Let’s start with the fee-only RIA. We give them $1,000,000 and they charge 1%. The fee calculation is simple. The fee will be $10,000 in the first year. The entire fee will be visible. Nothing will be hidden.

Let’s compare the fee-only scenario to a fee-based dual registrant who’s telling the client that they are a fiduciary. First, is the fee-based advisor a fiduciary, true or false?

The advisor is a fiduciary on the $500,000 fee-based account, but not a fiduciary on the $500,000 where they are using their insurance license to sell a variable annuity with hidden commission. This advisor is a dual registrant. The advisor is getting paid fees and commission. The problem is that you will not see the commission on the variable annuity.

You are going to see the 1% fee on $500,000, but you will not see the typical variable annuity commission which is going to be 7% on the other $500,000 which is a $40,000 commission.

Your fees in the first year will be $40,000. But wait, you’re only going to see $5,000!

This set up is very common with fee-based advisors who confuse you by telling you they are fiduciaries and then jam an annuity down your throat and rip you off using their insurance license.

Always remember, advisors who sell variable annuities are among the most selfish salespeople that exist.

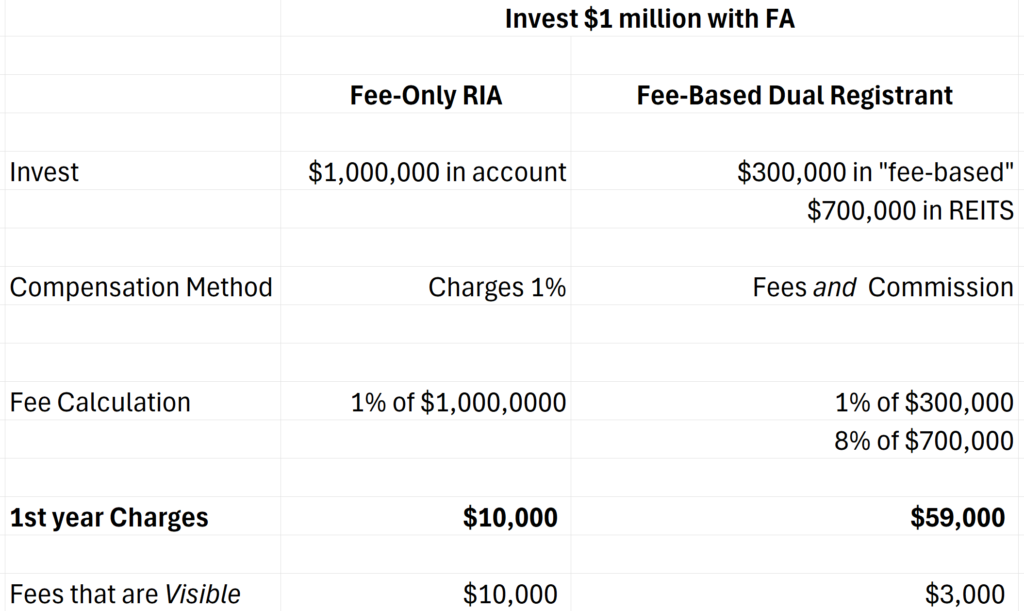

Fee-Based Financial Advisor Selling REITS

Our second fee calculation example is for a dual registrant who likes to sell private REIT limited partnerships. Same setup. The advisor is leading with a fee-based account telling the consumer, the client, that they are a fiduciary, but they are hiding significant commission in limited partnerships.

The hidden fees are substantial. The fee-based dual registrant advisor is receiving an 8% hidden commission on $700,000.

In the first year your fees are $59,000, but $56,000 in fees will be hidden from you.

It’s like magic. You are only going to see $3,000 in fees.

Meanwhile, advisers like this are telling you, oh, I’m your fiduciary, but what they are not telling you is that in your brokerage account where they are selling you these products, they are not fiduciaries and will be receiving huge commissions, none of which you get to see.

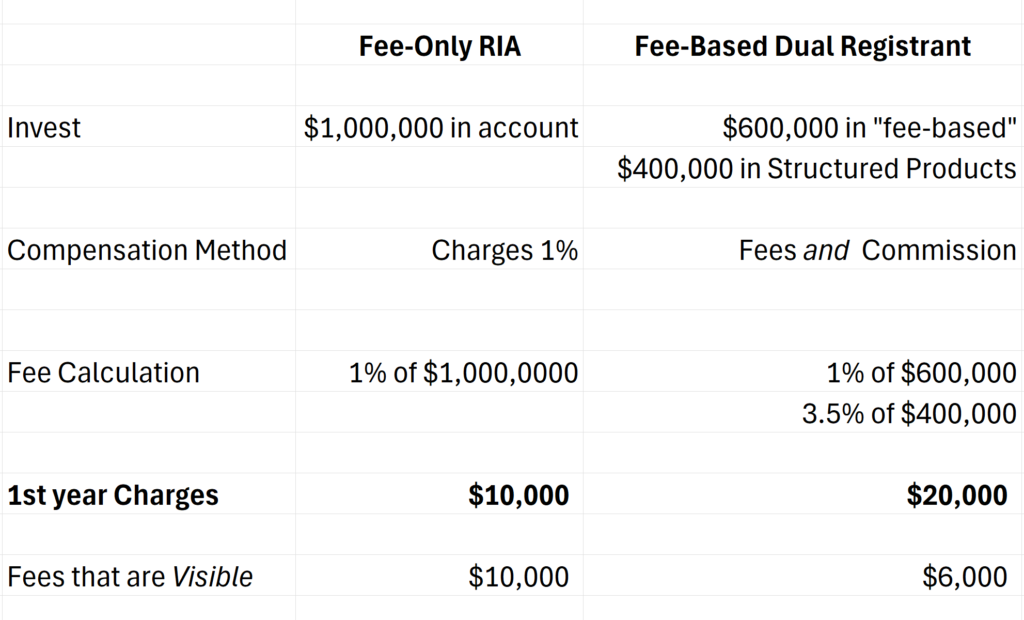

Fee-Based Financial Advisor Selling Structured Products

In this example our fee-based advisor is churning $400,000 of your money in structured products. The fee-based advisor confuses you by telling you they are a fiduciary, but the catch is that he is only a fiduciary on the $600,000 fee-based account. In the $400,000 account the advisor is taking you down for hidden commissions.

You are going to see a 1% fee on the $600,000. This account is where the advisor is acting as a fiduciary and saying that he is fee-based. But the advisor is going to hide the 3 1/2 percent commission on $400,000 of structured products.

Your total fees in the first year are going to be $20,000, but only $6000 is going to be visible.

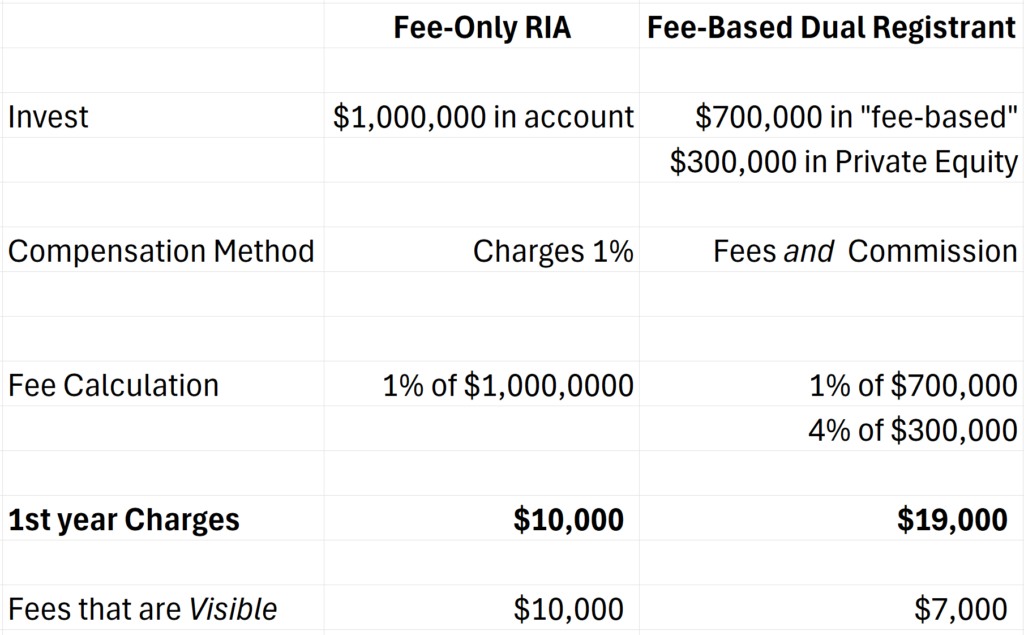

Fee-Based Financial Advisor Selling Private Equity

What if you have one of those sophisticated fee-based advisors that sells you some private equity? Wow, that sounds great doesn’t it? But guess what, they’re hiding the private equity commissions too. Yep, you do not get to see it.

Same situation, first year fees are $19,000, but you only see $7,000. To top it all off, they probably told you they’re a fiduciary!

Once again, the advisor is a fiduciary on $700,000 but not on the $300,000 where they’re hiding their fees and using their brokerage license to sell you a product.

You can be a cardiologist, tech entrepreneur, attorney, engineer, etc., i.e. a very smart person and still fall victim to this sales game.

I can not count the number of times I have seen this shakedown with fee-based advisors.

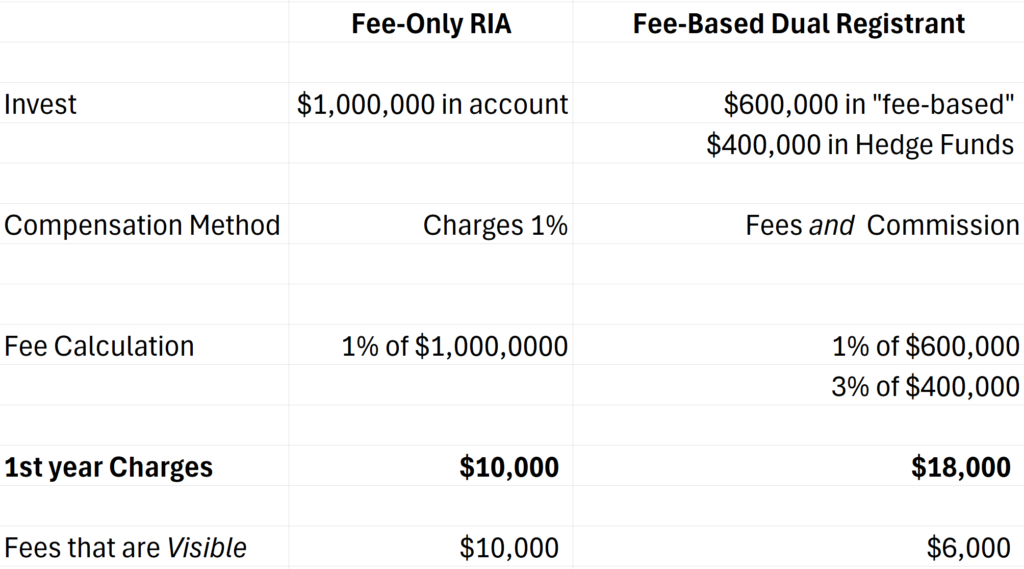

Fee-Based Financial Advisor Selling Hedge Funds

We would not be thorough if we left out hedge funds. You know those fancy investments that Warren Buffett thinks are worthless for good reason.

Here we have a fee-based dual registrant who once again is leading with a $600,000 fee-based account and telling you that they are your fiduciary. But simultaneously the advisor opens a brokerage account and uses their brokerage license to sell you $400,000 of hedge fund products.

The advisor is going to get paid under the table 3% commission that you don’t see and so your first-year fees are going to be $18,000 but you’ll only see $6,000.

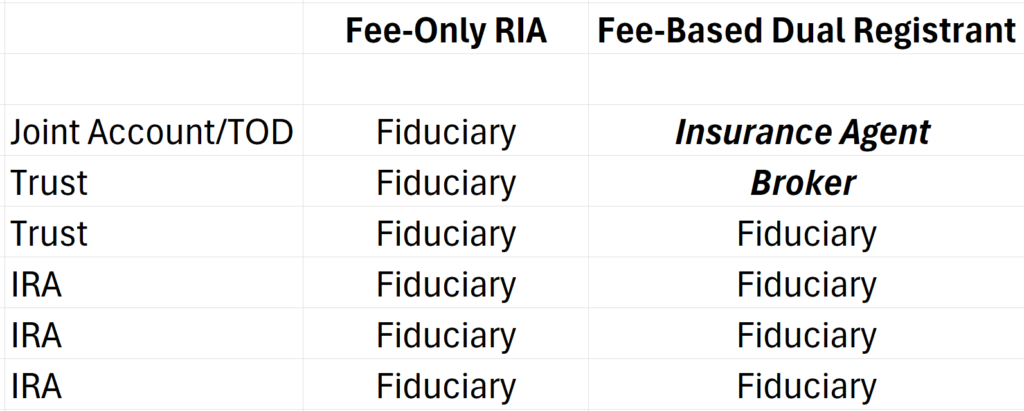

Fiduciary on One Account and Broker on Another

Here is an example that shows how fee based dual registrants play these games and get away with it legally. Often fee-based advisors will open multiple accounts for a client. Sometimes this is done to trick you. They tell you they are a fiduciary but then neglect to tell you that they are only a fiduciary on certain accounts. Then they churn your brokerage account with products for hidden commissions. The entire time you think you are working with a fiduciary and you are completely ignorant to the fact that you are being taken advantage of. This scam is by design. The advisor sells you on the fact that they are a fiduciary. But they do not tell you that they are going to be a part time fiduciary and acting as your broker on other accounts. Sophisticated shell game that happens every day to lots of savvy investors. I have seen this so many times it’s ridiculous.

In stark contrast, if you’re working with a fee only RIA, it’s real simple. The fee-only RIA is going to be a fiduciary on every single account one hundred percent of the time.

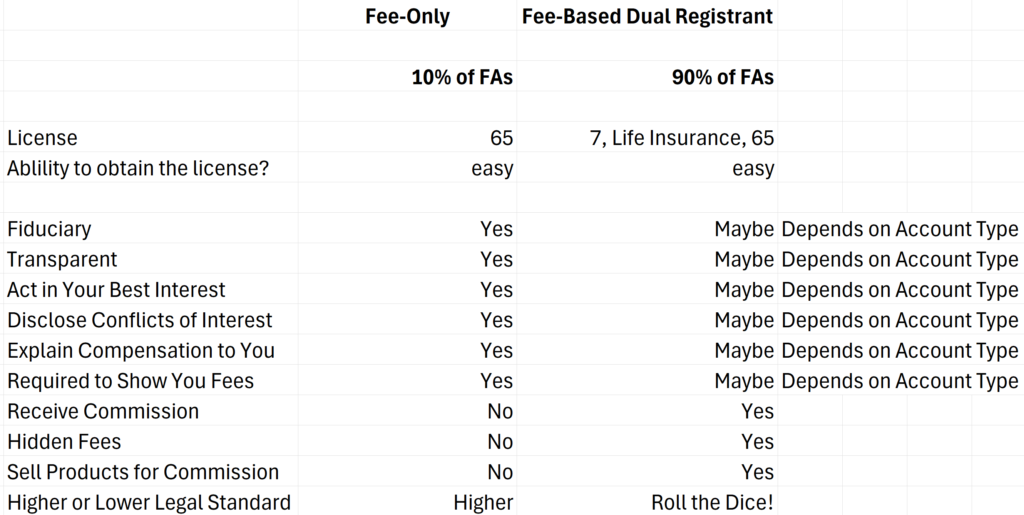

Here is is a summary table that shows the differences between a fee-only registered investment advisor and a fee-based dual registering financial advisor.

Fee-Only Fiduciary vs Fee-Based Financial Advisor

The differences are profound. Fee-based dual registrant financial advisors, have conflicts of interest, can hide their compensation, and can sell you products that are not in your best interest. With a fee-based advisor, they may be following the lower legal standard of suitability versus acting as a fiduciary.

I encourage you to familiarize yourself with these differences and learn why you don’t want to work with a fee based financial advisor.

No one wants to be taken advantage of. But the reality is that most fee-based advisors are nothing more than a wolf in sheep’s clothing.

They can take advantage of you in the blink of an eye and unless you are super sophisticated, you’re not going to know it.

The problem is that often the client is friends with the the fee-based advisor. They trust them. So they do not want to hear that they are getting taken advantage of. I have seen it so many times where a person is being taken advantage of and they just do not want to believe it. Also, there is nothing illegal about a fee-based financial advisor taking advantage of a client.

Someone who is registered as an investment advisor or stockbroker and an insurance agent can do what is in their best interest and not yours. They can legally do this to you and you do not really have any recourse.

If they have established suitability and they are selling you products, keyword products that are suitable, you do not really have a leg to stand on.

They can rip you off and can hide the commissions. There is nothing you can do about it.

You want to get away from this nonsense?

Find a fee only registered investment advisor who’s a fiduciary 100% of the time.

Always transparent and required by law to always act in your best interest.

Problem solved.

Ethan S. Braid, CFA

President

HighPass Asset Management

Denver, CO

This article is for education and illustrative purposes and is not tax, legal or financial advice. Your broker or advisor will charge you fees or commissions to make investments and therefore your returns will be less than indexes. For example, if you invest in the S&P 500 ETF, SPY, you will pay a fee to the company managing the ETF, State Street Global Advisors. Your return on the S&P 500 ETF, SPY, will be less than the SS&P 500 Index TR because of the fee paid to State Street Global Advisors. Additionally, you may pay a fee or a commission to your broker or financial advisor, further reducing your return, below the index. Consult your advisor or broker for a detailed list of their fees or commissions before you invest. Investing involves risk and you can lose money.