Investors have options for how they take retirement income from their portfolio. This article will review seven retirement income strategies every investor should know about.

Retirement Income Strategies

- Zero Coupon Treasury Ladder

- Fixed Systematic Withdrawal

- 4% Rule

- Immediate Annuities

- Variable Annuities

- Spending Dividends

- Rental Real Estate

Zero Coupon Treasury Ladder

A treasury ladder is a retirement income strategy where you purchase zero coupon treasury bonds maturing at set intervals for a specified period of time such as 10 or 15 years.

Pros

- Easy to Build

- Defined Retirement Income Stream

- State Tax-Free Interest

- Guaranteed by US Government

- Stepped-Up Basis at Death

Cons

- Taxes on Annual Interest Accrual

- No inflation Protection

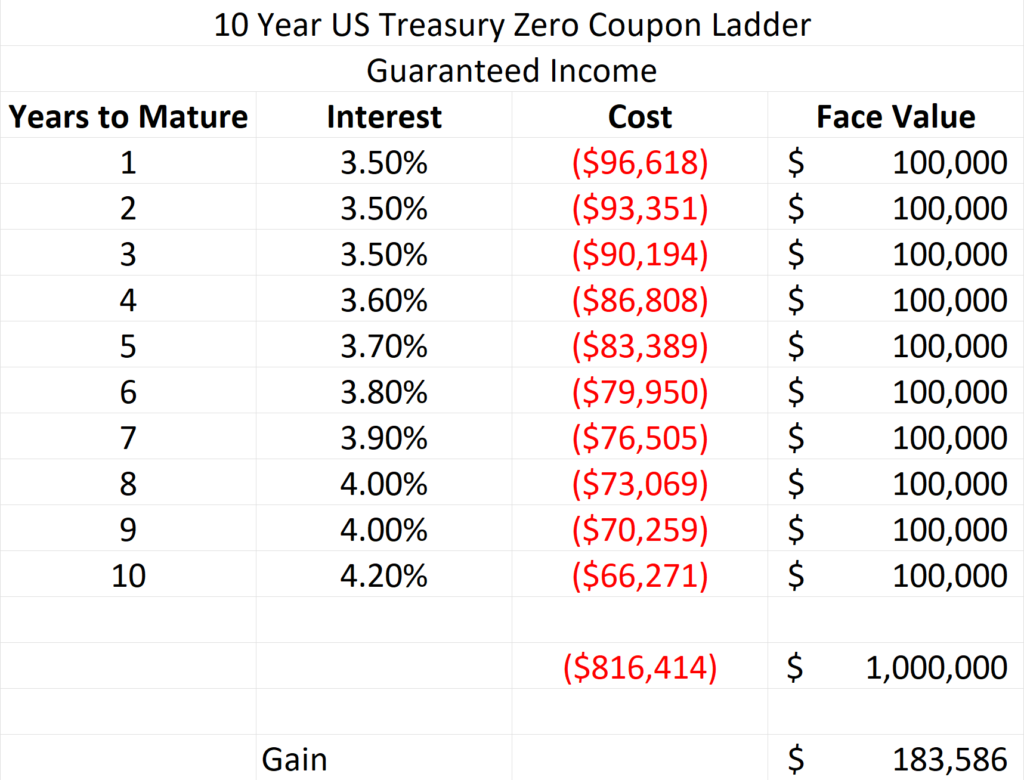

Treasury Ladder Example

In the example treasury ladder above the retiree will receive annual guaranteed retirement income cash flows of $100,000 per year for ten years. The cost of this guaranteed income stream is $816,414. The retire will earn $183,586 if they hold all of the treasuries to maturity. The interest rates are for illustration purposes, actual interest rates may be higher or lower depending upon market conditions. Investors need to know that zero coupon treasuries accrue taxable interest every year, but there is no interest received until the bond comes due. Investors holding zero coupon treasuries dated longer than one year will be responsible for paying taxes on interest that accrued but they did not receive.

Fixed Systematic Withdrawal

The fixed systematic withdrawal strategy is a retirement income strategy where you spend a fixed amount of your portfolio every year and do not raise the amount for inflation. Like a fixed pension payment, you will receive the same cash flow every year with no cost-of-living adjustment.

Pros

- Defined Retirement Income Stream

- Potential Appreciation of Portfolio

- Stepped-Up Basis at Death

Cons

- Asset Allocation Choice Influences Success

- Not Guaranteed

- No Inflation Protection on Withdrawals

- Market & Retirement Timing Can Limit Success

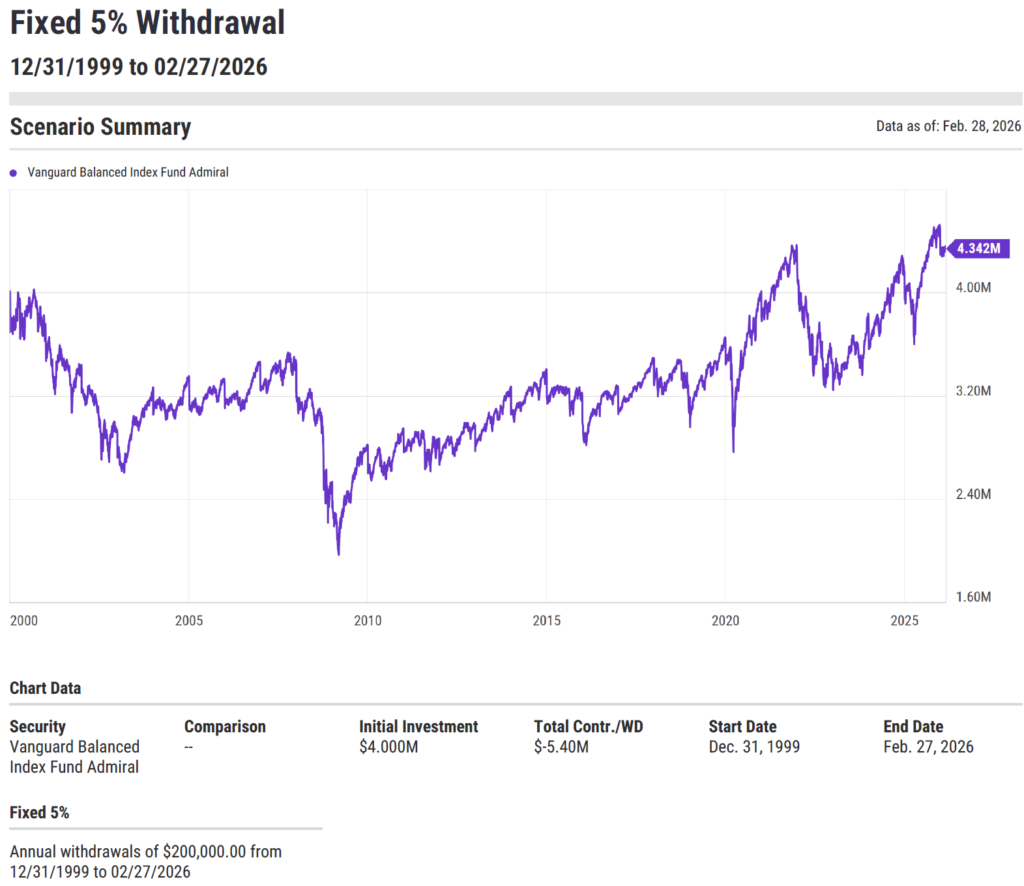

Fixed Systematic Withdrawal Example

In the hypothetical illustration above a retiree invested $4,000,000 in the Vanguard Balanced Index fund on 12/31/1999. The retiree withdrew a fixed $200,000 per year for 27 periods. A total of $5.4m was withdrawn. No additional fees or taxes were applied. After 26+ years, the retire has $4.3 million. I like this time period for analysis because it shows the impact of bad timing, retiring right before the recession of 2001 and incorporates the recession and crash of 2008.

4% Rule

The 4% rule is a retirement income strategy where you withdraw 4% of your portfolio in the first year of retirement and increase your withdrawal by inflation every year thereafter.

Pros

- Defined Retirement Income Stream

- Inflation Protection on Withdrawals

- Potential Appreciation of Portfolio

- Stepped-Up Basis at Death

Cons

- Asset Allocation Choice Influences Success

- Not Guaranteed

- Market & Retirement Timing can Limit Success

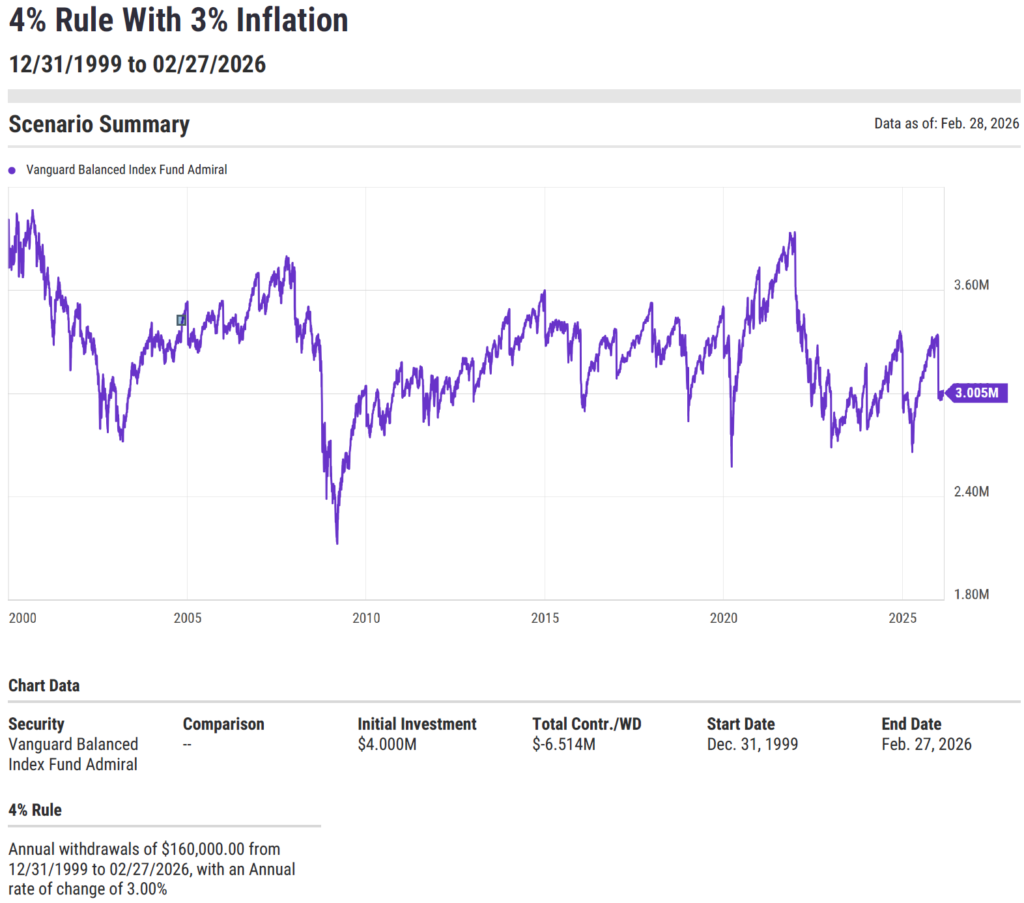

4% Rule Example

In the hypothetical illustration above a retiree invested $4,000,000 in the Vanguard Balanced Index fund on 12/31/1999. The retire withdrew 4%, or $160,000, in the year 2000 and then grew that distribution by 3% every year thereafter. Total withdrawals were $6.51 million. No additional fees or taxes were applied. After 26+ years they retiree has $3 million remaining in their portfolio.

Immediate Annuities

An immediate annuity is a contract with an insurance company. Immediate annuities provide guaranteed regular payments for a defined period such as 20-year period certain or lifetime joint and survivor. Investors using the immediate annuity retirement income strategy will purchase their annuity by making a lump sum payment to an insurance company.

Pros

- Guaranteed Income Stream

- Some Income is Tax-Free Return of Principal

Cons

- Low Rates of Return

- May Not Be any Funds Left for Heirs

- Taxable Income is Taxed at Ordinary Income Tax Rates

- No Inflation Protection

- No Stepped-Up Basis at Death

Variable Annuities

A variable annuity is a contract with an insurance company. Variable annuities are long-term tax deferred investments. Variable annuities can become a retirement income strategy when purchased with guaranteed withdrawal benefit riders also known as income riders. These riders allow you to spend a formula-based amount of your contract, for life.

Pros

- Potential Inflation Protection

- Riders Offer Guaranteed Cash Flow

- Potential Appreciation of Your Investment

- Some Income might be Tax-Free Return of Principal

Cons

- High Fees

- Taxable Income is Taxed at Ordinary Income Tax Rates

- Some Have Surrender Charges

- High commissions are Normal

- No stepped-Up Basis at Death

- Market & Retirement Timing can Limit Success

Spending Dividends

With this retirement income strategy, you simply spend the dividends generated by your passive investment portfolio. Your investments can range from individual stocks and bonds to ETFs and REITS.

Pros

- Potential Inflation Protection of Dividend Stream (Equities/REITS)

- Potential Appreciation of Portfolio (Equities/REITS)

- Dividends are More Reliable than Capital Gains

- Qualified Dividends are Taxed at Favorable Tax Rates

- Stepped-Up Basis at Death

Cons

- Higher Volatility with Equities and REITS

- Potential for Dividend Cuts

- Ordinary Dividends are Taxed at Ordinary Income Tax Rates

Rental Real Estate

Rental real estate is a widely used retirement income strategy. Investors have many options for rental real estate. Investors can purchase single-family rental homes, multi-family apartment buildings, strip malls, industrial buildings or office buildings.

Pros

- Depreciation Reduces Taxable Income

- Inflation protection from raising rents

- Potential Appreciation of your investment

- Diversification against stocks and bonds

- Increase profits by self-managing the property

- Stepped-up basis at death

Cons

- Loss of tenants

- Bad tenant who damages the property

- Tenant that does not pay

- Evicting a tenant

- Cost of ownership increases such as taxes and insurance

- Property maintenance costs

- Property manager fees

- Depreciation Lowers Basis

- Rental Income is Taxed at Ordinary Income Tax Rates

Summary

An investor’s choice of retirement income strategy will depend on their risk tolerance, time horizon, tax bracket and resources. Every situation is unique. Some investors will use only one retirement income strategy while others will use a combination of strategies. Your financial advisor will help guide you on which strategy makes the most sense for you.

Ethan S. Braid, CFA

President

HighPass Asset Management

Denver, Colorado

This article is for education and illustrative purposes and is not tax, legal or financial advice. Your broker or advisor will charge you fees or commissions to make investments and therefore your returns will be less than indexes. For example, if you invest in the S&P 500 ETF, SPY, you will pay a fee to the company managing the ETF, State Street Global Advisors. Your return on the S&P 500 ETF, SPY, will be less than the SS&P 500 Index TR because of the fee paid to State Street Global Advisors. Additionally, you may pay a fee or a commission to your broker or financial advisor, further reducing your return, below the index. Consult your advisor or broker for a detailed list of their fees or commissions before you invest. Investing involves risk and you can lose money.