Today I’m going to show you a simple way to quickly determine if $2 million is enough for your retirement. I’ve been a financial advisor for over 25 years and I have built hundreds of retirement plans. What I am about to show you is based upon that experience and that data set. To quickly determine if $2 million is enough for your retirement there are only two variables that we need to solve for.

- 1.) How much income can you realistically expect from a $2 million portfolio?

- 2.) How much cash flow do you need, what is your budget?

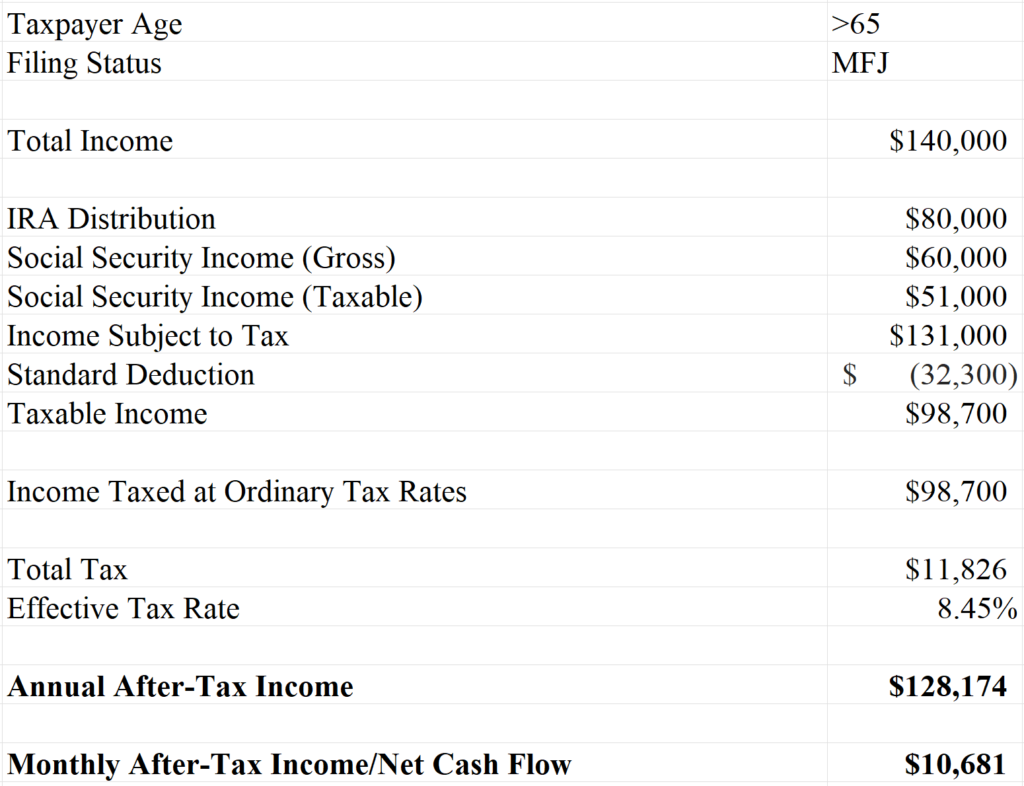

$2 Million Household Income Example

Let’s assume that your $2 million is in an IRA. A sustainable distribution from a $2 million IRA would be $80,000 in the first year, 4%. We’ve all heard about the 4% spending rule in retirement, so you simply take $2 million and multiply it by 4% in the first year and that is your sustainable income from your IRA. In addition to the IRA income, you’re going to have social security, so I’ve added $60,000 of Social Security. What I’m solving here is the net of tax amount that someone with a $2 million retirement portfolio and $60,000 of Social Security will receive. They will receive $128,100 net of tax.

So, if you are the typical family with $2 million in an IRA at retirement you can expect to receive a little over $10,000 a month net of federal taxes depending upon how much Social Security you’re receiving and any other pensions that you may be receiving.

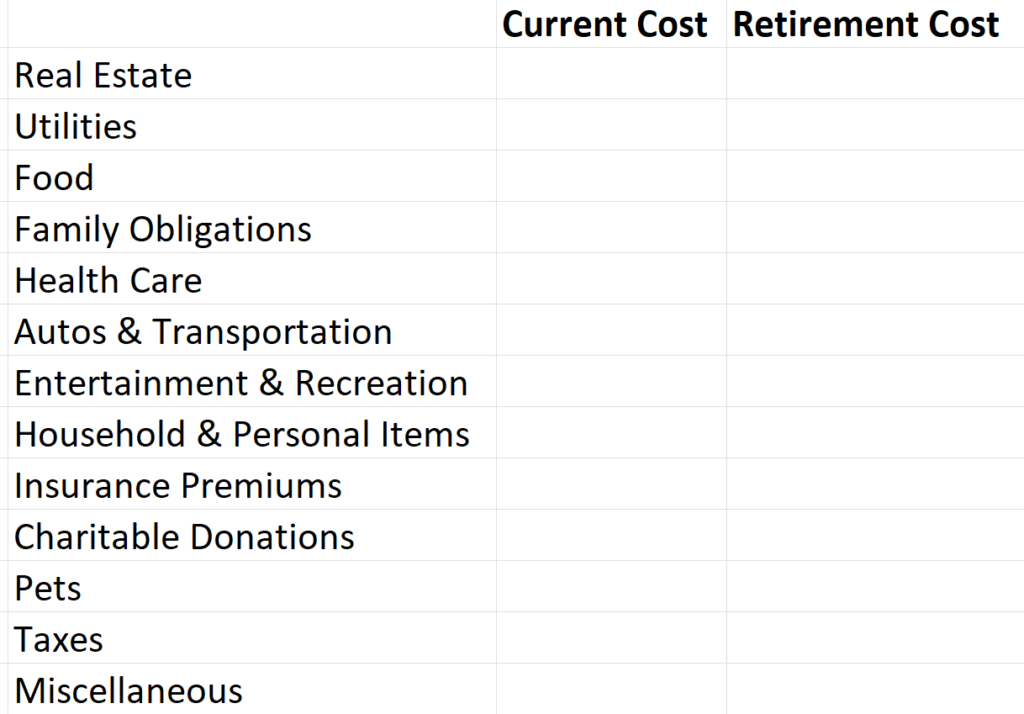

Preparing a Budget

Now let’s look at budgeting because the most important question is, does your sustainable income cover your budget?

I think it’s best to cast the net as wide as you can and start with big picture categories like real estate, utilities, food, family obligations, healthcare, autos, etc. Once you have filled out your current cost you want to estimate as best as you can what you think your retirement costs will be so that you have a very good idea of what your retirement lifestyle cost will be.

You can get as micro as you need to for each of those big categories.

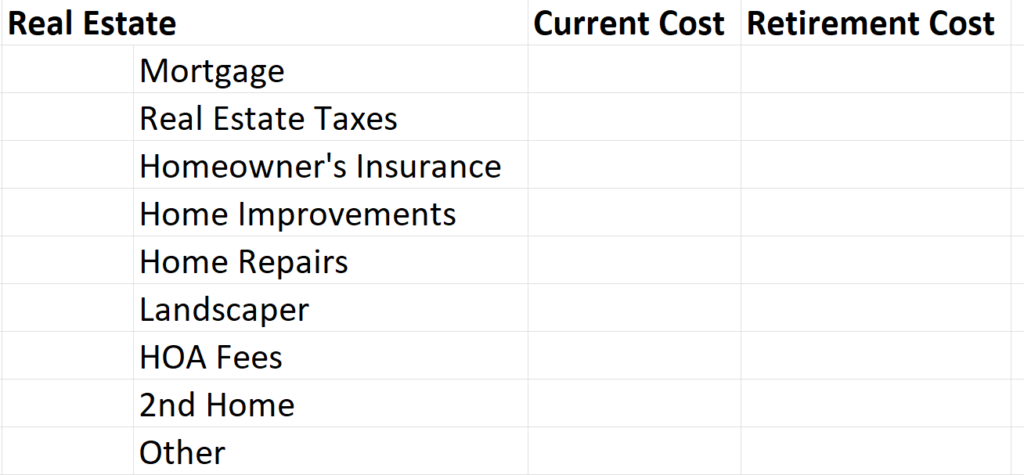

For example, with real estate, what is the mortgage, what are your real estate taxes, what is your homeowners insurance, what are home improvements and home repairs looking like? But I think it’s best to start with the big picture and then get micro if you need to. Ultimately you want to develop the most accurate budget that you can when planning for your retirement.

Reconcile your Budget with your Expected Income

Once you have your budget in place you simply reconcile that budget with the monthly cash flow that you expect to receive from your IRA and Social Security. For example, if you anticipate receiving just over $10,000 a month from Social Security and your IRA but your budget is $11,000 you have a problem. If on the other hand you’re receiving $10,000 a month from your IRA and Social Security but your budget is only $8,000 you’re in a great situation.

In my experience with many years of planning I always tell people it’s better to plan for the unexpected than to cut it too close. What I mean by that is if you anticipate receiving $10,500 a month on a net basis after taxes as a monthly income stream from your portfolio and Social Security then you really don’t want your monthly budget to be more than say $9,500. I recommend you leave yourself $1,000 of flexibility in your budget and that will allow you to save some cash in a savings account throughout the course of the year to handle the unexpected things that will happen in your retirement. You can be sure that things like appliances breaking, hail damage, insurance deductibles, etc. will eventually occur and you want to be prepared!

Ethan S. Braid, CFA

President

HighPass Asset Management

Denver, CO