Retirees should plan to encounter four recessions during a typical 25-to-30-year retirement. According to Fed Chair Jerome Powell during his March 19th, 2025, press conference, the unconditional probability of a recession is in the range of 1 in 4 at any time. Another way to determine the unconditional probability of a recession is to divide the number of recessions that have occurred in the last 100 years by 100. Since there have been 15 recessions in the last century, your unconditional odds are 15% by this method. Whether we use Jerome Powell’s math or the recession frequency of the last century, we can conclude that recessions are real, and they do happen. If we take the midpoint of the two statistics, you have an approximate 1 in 5 chance of a recession in any given year.

Why Four Recessions?

Most retirees will plan for a 25-to-30-year retirement. With recessions occurring on average every 5 to 7 years, you should expect at least four recessions during a normal retirement. The timing of recessions can be erratic. You may see two recessions in three years like the early 1980s and then go for many years with no recession. Use probability as your guide. Plan for four recessions over your retirement and be prepared for them to show up, randomly, in any given year.

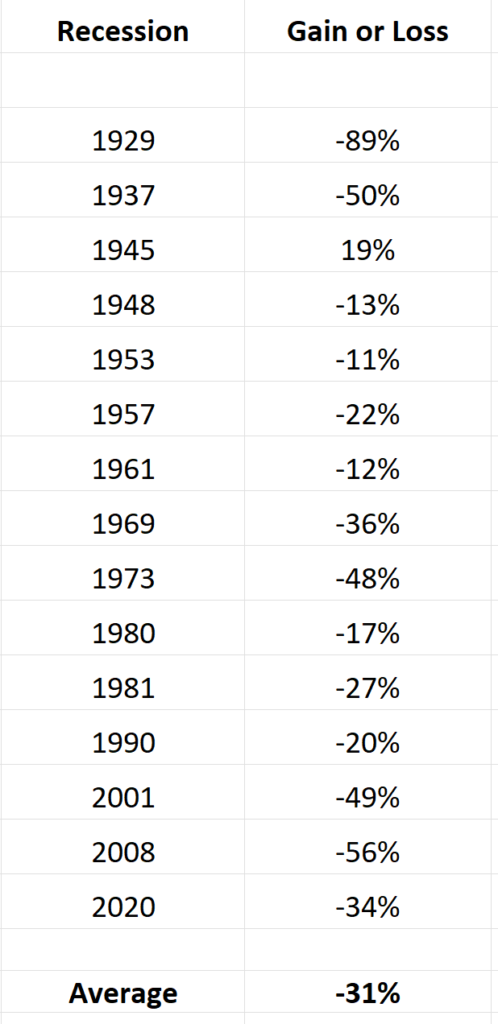

How Much Do Stocks Lose in a Recession?

In the table below we see that the average peak to trough loss for the S&P 500 and it’s predecessor index is (31%) during a recession. Not all recessions have been associated with a loss in the stock market. During the recession of 1945, the S&P 500 went up during the recession!

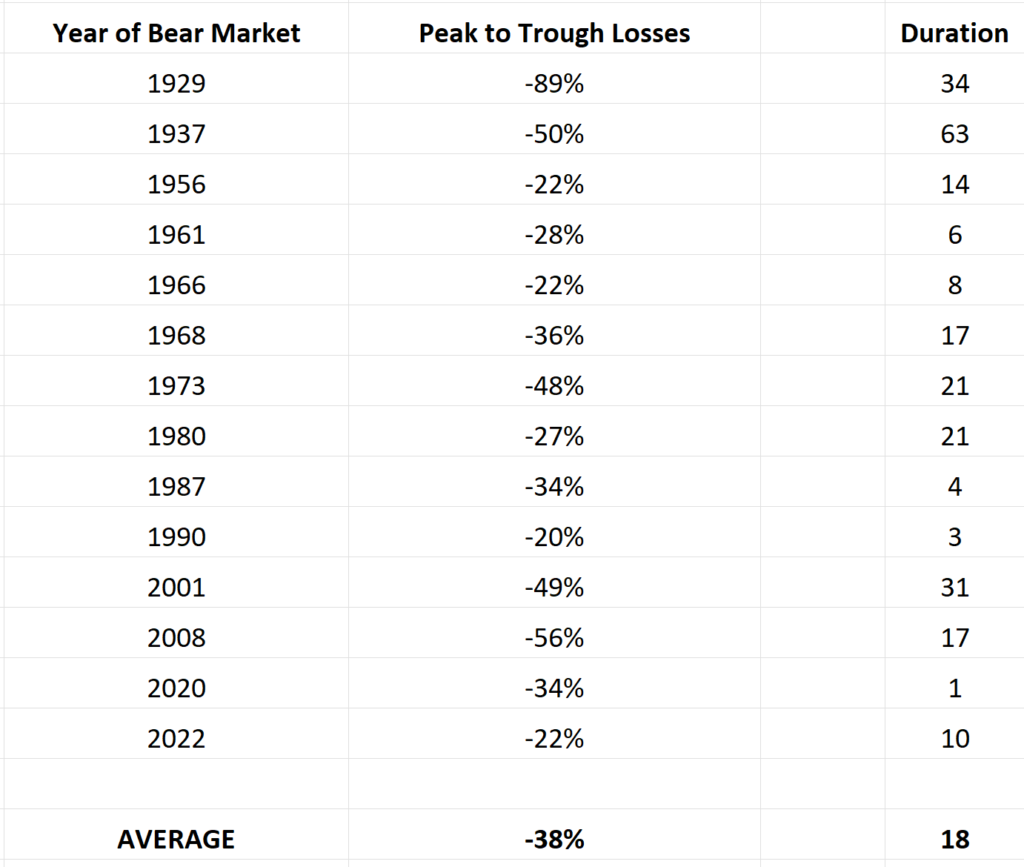

Bear Markets Can Occur Without a Recession

Bear Markets, defined as a loss of (20%) or more, are often associated with a recession but can occur randomly too. For example, the bear markets of 1987 and 2022 were not associated with a recession but in both cases, investors lost a considerable amount of money in a short period. We have experienced 14 short-term bear markets in the last century. The unconditional odds of a bear market happening in the year you retire are like the odds of a recession.

What Happens With Bad Timing?

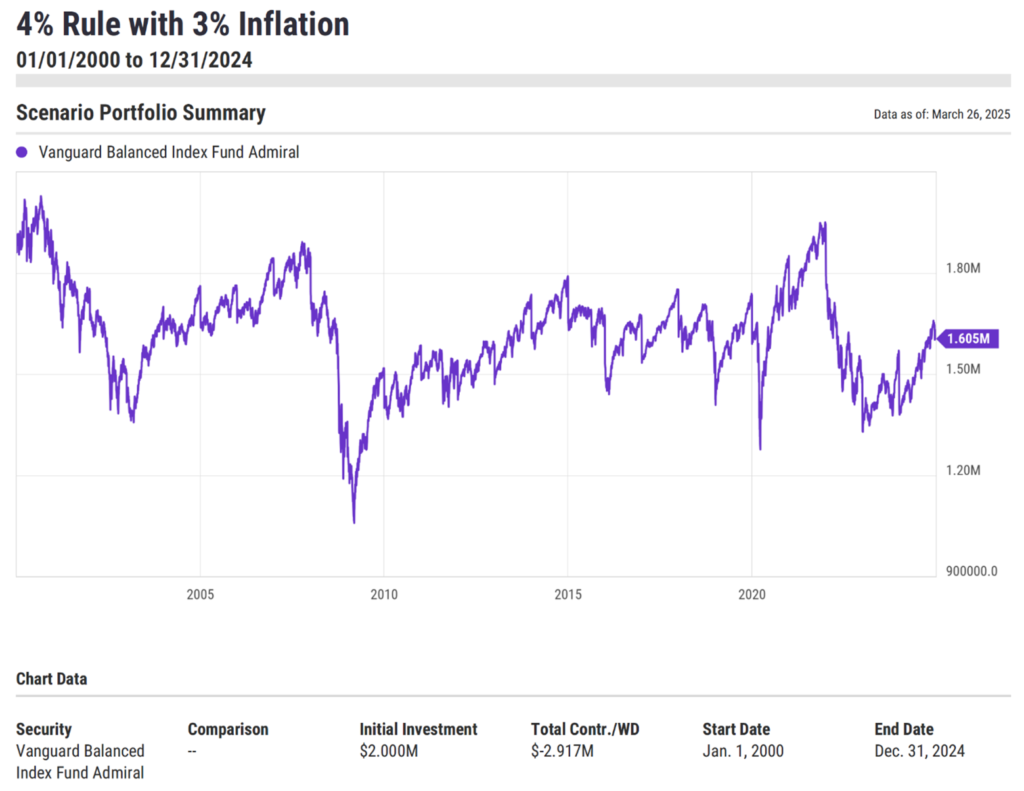

If you have bad timing and retire right before a recession, you won’t know until it is too late. Most likely you will lose money and potentially a lot of money. If your portfolio is heavy on stock market exposure, you may jeopardize your retirement plan. The illustration below is for a person who retired on January 1, 2000. The retiree invested $2 million in the S&P 500 Proxy ETF, SPY. The retiree used the inflation adjusted 4% rule for spending. In 2023, the retiree ran out of money. Bad retirement timing combined with an all-equity portfolio was too much strain on the retiree’s assets

How Can You Protect Yourself?

Asset allocation is an effective tool for reducing portfolio volatility. Lowering volatility can help protect you from the effects of bad timing in retirement. The illustration below is for a 60/40 equity/fixed asset allocation fund. In this illustration, our retiree invested $2 million in the Vanguard Balanced Index Fund on January 1st of 2000. The retiree used the inflation adjusted 4% rule for retirement spending. Unlike the prior illustration where bad timing with an all-equity portfolio resulted in the retiree running out of money, this retiree still has $1.6 million after 25 years of retirement.

Ethan S. Braid, CFA

President

HighPass Asset Management

Denver, CO

This article is for education and illustrative purposes and is not tax, legal or financial advice. Your broker or advisor will charge you fees or commissions to make investments and therefore your returns will be less than indexes. For example, if you invest in the S&P 500 ETF, SPY, you will pay a fee to the company managing the ETF, State Street Global Advisors. Your return on the S&P 500 ETF, SPY, will be less than the SS&P 500 Index TR because of the fee paid to State Street Global Advisors. Additionally, you may pay a fee or a commission to your broker or financial advisor, further reducing your return, below the index. Consult your advisor or broker for a detailed list of their fees or commissions before you invest. Investing involves risk and you can lose money.